Interest Rates, Faith, and Democracy

What a pickle!

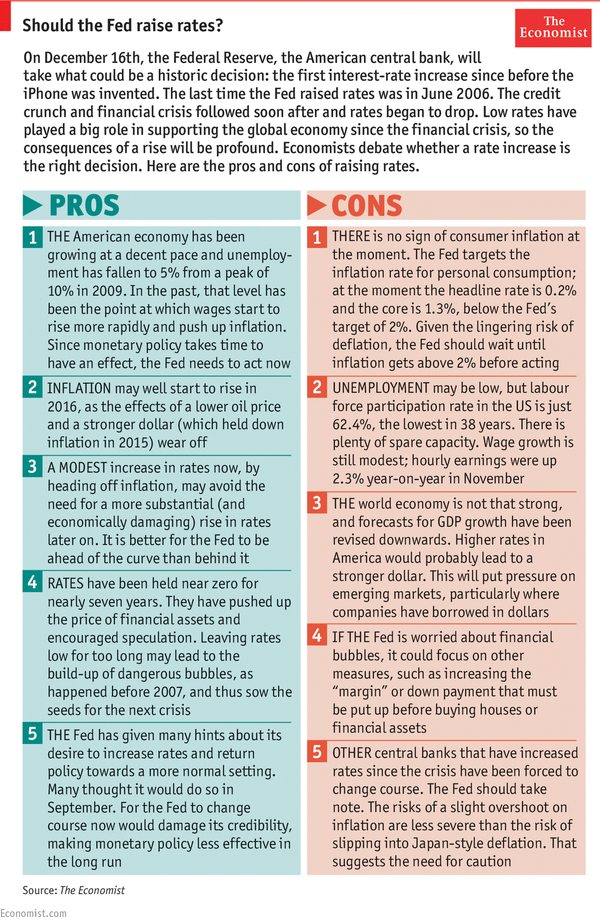

The Federal Reserve Board’s meetings have become a media event. The last few days – weeks if you want to be more inclusive – have been awash with media chatter and analysis about the probability that the Fed will, at last, raise interest rates. As a public service here are the pros and cons as seen through the eyes of the Economist:

And here, in its entirety is a letter to the editor of the Financial Times just yesterday from someone called Thaddeus Walkowicz, who lives in East Hampton, New York:

Fed’s focus on creating jobs comes at huge cost to the rest of US society

“Sir, Although is universally described as the “smartest man in the room”, Lawrence Summers’ article on “neutral interest rates” (Central bankers do not have as many options as they think”, Dec 7) is simply a part of the nest chapter of trying to perpetuate failed Keynesian perspectives and a desperate attempt to institutionalize acceptance of “observations” that masquerade as policy-justifying “research”.

As developing countries grab a greater share of world gross domestic product through the provision of cheap labor, governments and central bankers of the industrialized west have resorted to “serial stimulus” to try to achieve historical levels of growth, almost as if their countries were entitled to the levels of growth. The accompanying monetary stimulus has driven down real interest rates, and these rates are now included as data points with the perverse circular narrative that the lower levels represent some form of appropriate “real rate equilibrium”. (This is indeed true if generational theft is an integral part of policy.)

Ignoring the theft of senior’s savings imparted by negative real interest rates, completely missing from Professor Summers’ article is any discussion about the effects Generation X’s and Millennials’ savings required for retirement, with the negative real rates and lower risk premiums on all asset classes, and more importantly what this means for current and future spending/growth.

It’s time to face the music: the simple reality, as harsh as it may be for those without marketable skills or even PhDs and for central bankers protecting an “intellectual” legacy, is that an overextended focus on job creation is not worth the long-term cost to the rest of society in terms of the continued upheaval of a free-market economy, one characterized by a fair, market-driven balance between lenders and borrowers.”

Wow.

Interest rates, faith, and democracy all bound up in one big spewing forth of anti-economics venom.

Tell us what you think Thaddeus.

It’s hard to know how to respond, but I want to pick out a few points.

First, Thaddeus clearly has a deep disregard for economics. In this I must admit he is not alone. Just yesterday Lars Syll referred to a book by Dani Rodrik and explained that Rodrik’s comments were more about economists than the substance of their work. Here’s what Syll said:

“There’s much in the book I like and appreciate, but there is also a very disturbing apologetic tendency to blame all of the shortcomings on the economists and depicting economics itself as a problem-free smorgasbord collection of models.”

This is what Thaddeus is saying too. Only with less precision. If we view economics as an array of models to be taken out and deployed whenever we wish, then we rapidly approach the “observations” that masquerade as policy-justifying “research” that Thaddeus dismisses rather contemptuously. After all such an array does start to look an awful lot like a whimsical toy-box full of goodies that an economist can take out and play with arbitrarily. What, a quizzical onlooker might well ask, determines which model we deploy? An examination of the facts? if so, which facts? What triggers are we responding to? What is our desired goal? The sad matter is that economics has many models for most occasions and the choice can, indeed, appear arbitrary.

Worse, it can appear faith-based or ideologically driven.

Back to Thaddeus’ letter: I like the way he dismisses Keynes as being a “perspective”, or, rather, a “failed perspective”. He doesn’t even dignify Keynes as having produced a theory or the kind of model Rodrik talks about. That’s pretty low. But it fits neatly with a right of center narrative that markets are natural phenomena that we meddle with at our peril. Poor old Keynes might have thought he was saving capitalism from itself, but he doesn’t get many thanks from our capitalist class.

Just for the record: markets are social constructions that occasionally display “law-like” behavior, but they are profoundly human and thus exhibit all our human frailties.

I also like the”theft” concept that Thaddeus tosses about. It’s clear that in his eyes low interest rates are a form of theft. With the aggrieved party being, presumably, anyone who is saving or has saved for retirement. That’s my best spin. I suspect though that underneath the surface Thaddeus is really making a statement on behalf of rentiers everywhere: how’s a good rentier to make a buck in this low rate environment?

Thaddeus also seems to have bought into secular stagnation. He doesn’t mention it explicitly, but the idea lurks behind his suspicion that central bankers are trying to pump up growth because it’s “almost as if their countries were entitled to the levels of growth”. Naughty industrial countries! Such entitlement. Only rentiers are allowed to have real entitlements.

Speaking of which: Thaddeus clearly holds every day workers in even more contempt than he does economists. His apparent reference to the days of growth being gone and to the speciousness of attempts to create jobs speaks volumes for his empathy for his fellow citizens.

The sad part Thaddeus is not alone. His lack of empathy is matched and often outdone by economists who have fallen foul of the “laws” of economics. If you believe – have faith in – in the natural nature of the economy and ignore its human origins, if, in other words, you tend to refer to people as “agents” or “units” or any other elision of their human reality, it is quite possible to look upon job creation as a false activity. What you are likely to be more focused on is the urgency of avoiding debasement of the currency and the preservation, at all costs, of faith in the value of the dollar. In other words the Fed needs to fight inflation, and not to worry about jobs. Especially for those “without marketable skills”, as Thaddeus so amiably puts it.

When I read letters like this I wonder how it was that mainstream economics became so resolutely anti-democratic. Perhaps that’s too harsh. Perhaps it is just that the “natural laws” that drive the economy are so anti-democratic, and economists are simply swept along by their observation. In this narrative economists are only the bearers of bad news, constantly telling us that our lives are subject to the great machinery of supply and demand and not at all to human intentions and/or interventions.

I suppose that all this is simply my way of saying that when I approach that smorgasbord of models I look first for those that preserve democracy and tend to shun those that undermine it.

Which brings me all the way back to interest rates: yes, I think the Fed will raise them. No, I don’t agree – there’s too much downside risk. Yes, the Fed ought to focus on job creation – its the democratic thing to do! And, by the way, looking back into history we find that the so-called “normal” and thus higher rate levels rentiers are pining for are the exception not the rule. Low rates are here to stay.

Well that’s what some of the models say. As for the other models …

You see what I’m saying?